All Insights

Ooh, I've been loving you too long / I don't wanna stop now, oh / With you, my life has been so wonderful / I can't stop now

Otis Redding. Lyrics to I’ve Been Loving You Too Lond, 1967

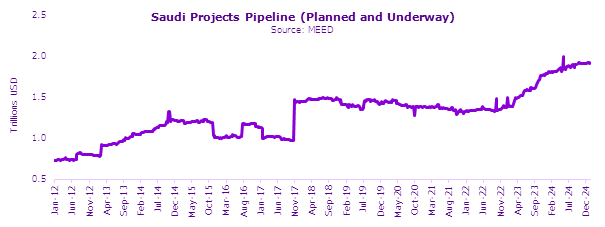

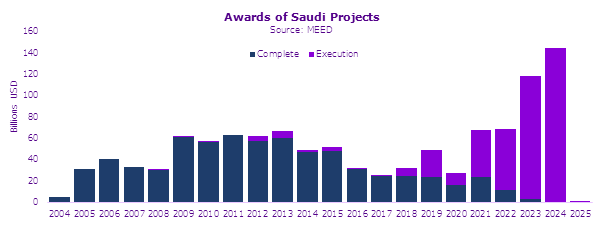

Since Vision 2030 related investments started to accelerate in 2021, Saudi’s domestic manufacturing industry boomed as it fed demand for cables, transformers, switches, transmission towers, pipes, steel beams, and more. Listed industrial companies repaired balance sheets wounded by a decade of domestic underinvestment and saw profits surge from 2022-24. Many companies paid their first dividends in a decade in 2024 and more will follow in 2025. And while such industries are inherently cyclical, that the cycle continues to prolong is the view of the numerous management teams we speak with in the sector.

Saudi’s commitment to developing domestic gas pipelines from their newly productive gas projects like Jafurah created first order effects for demand for oil & gas services, and a second order effect of strong demand for pipeline infrastructure to deliver the gas domestically. The third order effect of widely available gas is intended to support an evolving manufacturing sector throughout the kingdom, envisioned as a driver of FDI. On our visit to NEOM in November, we learned that these East West gas links will be critical for the FDI (green materials manufacture) required to develop infrastructure at NEOM over the next 20-30 years. Moreover, as Saudi actively negotiates tech transfer agreements to allow things like air conditioner compressors and passenger vehicles to be manufactured in Saudi Arabia, these factories will require energy, and that energy will be largely gas derived.

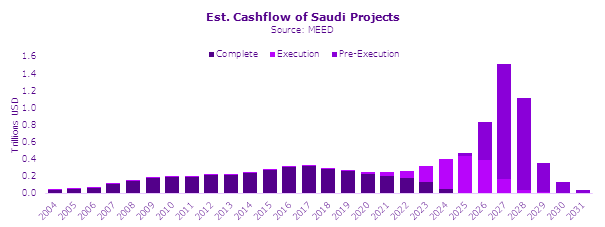

In 2025, our team is focused on understanding what Infrastructure 3.0 looks like in Saudi; as the growth in power and water generation moves into project execution and operation, what can domestic manufacturers evolve to provide? Unlike in the developed world, where data centre projects are powered by existing de-industrialised power spare capacity, that lack of spare capacity in the GCC and in Saudi in particular means that access to power and water remains in short(er) than desirable suppl , and to address the demands of digitisation, far more power and water will still be required. Perhaps this explains the meteoric performance (untethered from fundamentals, in our view) of ACWA Power, which is up 462% since its 2022 IPO and over 60% in 2024.

Data centres are an area where we spent significant time building our knowledge base in 2024, and in many ways, we now understand them as the infrastructure that will enable the digital economy, digitised lifestyle, and leisure-service driven future the GCC envisions for itself. Critically, as mentioned above, Saudi’s investment in oil & gas extraction is now principally focused on powering its domestic industries. Although exports of oil, gas, and petrochemicals remain critical, the government intends that the marginal buyer of future energy production should be more local than global.

Critically, this infrastructure investment runs alongside significant commitments to ‘soft’ infrastructure development in tourism, entertainment, healthcare, education, and commercial services – enabling the Saudi government to continue its drive to grow non-oil GDP.

We are stardust / Billion year old carbon / We are golden

Joni Mitchell. Lyrics to Woodstock, 1969

We see 2025 as the breakout year for Saudi tourism, both religious and secular, both domestic and inbound international. While a Saudi ‘Woodstock’ has yet to be announced, it’s no longer out of the question, with each week in Saudi bringing new exhibitions of art both high (art biennales and transcendental evenings of music aplenty) and low (all the WWE and monster trucks you can handle!) Moreover, as Ramadan and Hajj (which move 11 to 12 days earlier annually) shift into the winter months over the next 15 years, opportunities to safely accommodate more pilgrims in much expanded sites in Mecca and Madinah abound. As we have mentioned in previous letters, increasingly the organisation and stewardship of these pilgrimages is privatised and run by Saudi companies rather than directly being the onus of the government. As Saudi moves towards its targets of 30 million pilgrims (compared to 8.5 million Umra Pilgrims in 2019) and 150 million international tourists, as well as 330 million annual air passengers by 2030 (vs 128 million today), both the weather and their share of tourist activity bode well for Saudi’s tourism industry. Tourism is also a key employment focus and perhaps the sector best aligned with the Kingdom’s vision for a modern, outward facing, service-oriented workforce.

During 2025, we expect the IPOs of several existing tourism businesses, with Flynas, the country’s longstanding low-cost carrier chief among them. In addition, Riyadh Air, Saudi’s answer to Emirates, Etihad and Qatar Airways, will launch out of Riyadh, Boeing delivery challenges notwithstanding. Simultaneously, we will see the grand opening of 4 ultraluxury sites on the Red Sea, 3 at Red Sea Global (south) and 1 at NEOM (Sindalah, north). Having spoken to the management teams of several of these properties as well as to some early guests during their soft openings, the resorts represent Saudi Arabia’s attempt to draw a share of the growing global ultraluxury market, with exclusive, remote, and pristine hospitality offerings. In a world beset with messages about dry January and the perils of alcohol, we were unsurprised to hear early visitors (hailing from the US and Europe) brushing off the lack of alcohol completely, and in fact commenting that this was a plus!

From a regulatory perspective, we expect significant announcements to bolster the Saudi tourism market in 2025, from regulations around foreign ownership, to alcohol, to wider allowances for sporting and artistic events. Perhaps no change is more anticipated than that to foreign ownership both of companies with assets in Mecca and Medina and of real estate assets in the cities themselves – foreign ownership restrictions to public shares of the companies in question were lifted this past month. Amongst Saudis, the expectation is that full foreign ownership regulations in the country are imminent, as both a driver of FDI and as an avenue to allow Saudis to liquidate longstanding holdings and reinvest in new growth areas in the country.

\

Further Reading

\

Get the latest insights

We share perspectives, research, and market insights to help investors and founders see where growth is emerging — and how to capture it. Discover what others might be missing.

Investment Manager: Ajeej Capital (DIFC) Limited, regulated by the Dubai Financial Services Authority (DFSA). Ajeej Capital (AD) Limited regulated by the Financial Services Regulatory Authority (FSRA) of Abu Dhabi Global Market (ADGM). FSP No. 180021. © Ajeej Capital 2026

.avif)