All Insights

“I’ve spent a lifetime / waiting for the right time … the time is here at last”

Elvis Presley. Lyrics to It’s Now or Never, 1960

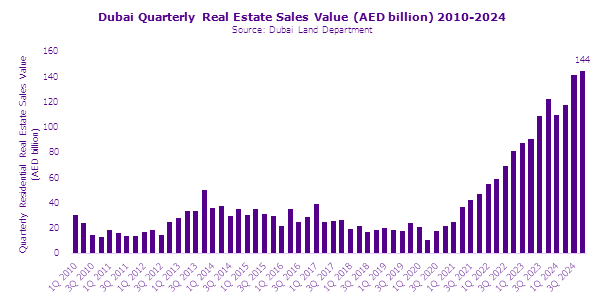

If Dubai’s real estate agents moonlighted as Elvis impersonators (and some in fact do), this would be their song. In 2024, Dubai’s real estate market reached heights little anticipated by even the market’s largest developers. Calls to attend property launches, to sell their existing properties, and even to sell properties they’d purchased that are still under construction inundated the entire team. Every day, it seemed, brought a new unsolicited real estate agency to our WhatsApp chats, and every week brought a new property launch or three.

Despite the travails of property market cycles past, this cycle really has evolved differently, largely because of the regulatory framework built over the last decade by RERA in combination with the population inflow driven both by the push factors of geopolitical instability and macroeconomic headwinds, and the pull factor of Dubai’s ever improving quality of life. As we often explain when abroad, over the past 17 years, Dubai’s roads, regulations, and restaurants have all gotten a lot better, while in other global cities, the same 3 elements have gotten a little bit worse, closing a critical gap.

Closing the quality gap and throwing the doors to migration ever wider made 2024 the year that Dubai achieved escape velocity that moved the city-emirate firmly into the orbit of global cities. Over 150k residential units were sold in Dubai in 2024 and close to 300k changed hands throughout the UAE, as the property markets in the emirates of Abu Dhabi, Ras Al Khaimah, and Sharjah also meaningfully accelerated and matured. As the year passed, buying activity increasingly shifted to smaller units and towards investors, a natural evolution that indicates that the property cycle is in fact toppish, but that strong UAE-wide consumption growth is likely to sustain as homes are completed and dampen further price and rent increases.

Notably, relative property prices and rents in Dubai remain lower than other leading global cities, but incomes cannot sustain significant further price growth, even with the injection of ~500k higher income residents over the past 3 years. Thus, the focus shifts now to completion and handover of projects and the government’s significant investments in new infrastructure (roads, as mentioned earlier, but also power, water, cooling, schooling, and health facilities) to support the development of the new suburbs south and east of Sheikh Zayed Road – Dubai’s central artery. Unlike in previous cycles, the developers and managers of these infrastructure projects, today, form part of the public equity market, providing an avenue for investors to directly benefit from Dubai’s wider economy.

\

Further Reading

\

Get the latest insights

We share perspectives, research, and market insights to help investors and founders see where growth is emerging — and how to capture it. Discover what others might be missing.

Investment Manager: Ajeej Capital (DIFC) Limited, regulated by the Dubai Financial Services Authority (DFSA). Ajeej Capital (AD) Limited regulated by the Financial Services Regulatory Authority (FSRA) of Abu Dhabi Global Market (ADGM). FSP No. 180021. © Ajeej Capital 2026

.avif)