All Insights

.avif)

Dear Investors and Friends,

2025 proved to be a year of contrasts for our flagship strategy. The Ajeej MENA Fund (AMF) ended the year essentially flat at +0.4%. This performance unfolded against a deeply bifurcated regional backdrop: while the MSCI Arabia NR returned 7.1%, its largest constituent, Saudi Arabia (representing over half the index), slid -12.8%.

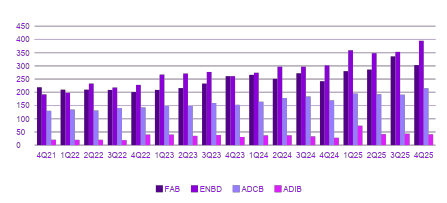

The AMF benefitted from positive returns on stocks exposed to Dubai and the UAE’s population and economic growth, including Salik, Parkin, DEWA, Emaar, and FAB, as well as Saudi financial and industrial exposures. This was offset by negative contributions from some of our longer-term convictions, namely Talabat in the UAE (see below) and certain exposures in Saudi including insurance and IT names. The MSCI Arabia NR index’s headline growth was driven primarily by Kuwait and Dubai, which gained 21% and 17% respectively, as well as by Abu Dhabi banks which outpaced the Abu Dhabi market’s 6% return. The smaller MENA markets of Egypt, Morocco, Jordan, and Oman also had a strong year and contributed in aggregate nearly 2% of the 7% index return – the first two markets benefitted from an additional tailwind from USD weakness during the year. While some markets and stocks did not perform as well as we anticipated during 2025, the variation in performance helped to provide fertile ground for building high-conviction, long-term allocations.

As a benchmark-agnostic fund, our performance often reflects the timing of our deepest convictions. In 2025, this was most evident in Talabat. Following its underwhelming December 2024 IPO, we moved against the grain, consistently adding to our position as the stock retreated.

We spent much of the year stress-testing our thesis, specifically regarding the entry of Keeta (owned by Meituan). The prevailing market consensus is that Keeta will aggressively erode Talabat’s profitability. We fundamentally disagree.

The market’s bearishness is largely an inference drawn from Keeta’s entrance into Saudi Arabia, where it significantly impacted Jahez, as well as from its track record in its home market. We believe these comparisons are flawed for several reasons:

While we anticipate some margin compression as these markets mature, our confidence in Talabat’s long-term top-line growth remains steadfast. We view the current market scepticism as a disconnect between short-term noise and long-term fundamental strength.

One of the most frequent questions we hear from investors has to do with their curiosity about the ultimate ‘aims’ of the GCC leadership class – and note here we say ‘class’ not ‘rulers’ because the first clarification necessary is that the titular heads of this region are supported by a vast class of friends, relatives, rivals, business partners, and philosophers whose council they seek on an ongoing basis. It’s rule by consensus, not fiat. When we explain that those aims are to establish societies (to play off the hideous HSBC jetway adverts) that are open yet highly organised, mercantile and yet generous, and growth-focused yet enamoured of their own history, cosmopolitan and yet traditional, our answer generates a further cascade of questions – both the, “how can these tensions live unresolved?” and “how can we get involved investing in such a place?”

The simple answer, of course, is ‘come and see,’ and over the past year our firm has welcomed an increasing number of current and potential investors to our offices in Dubai and served as their guides to our region both in the UAE and beyond. The complex answer as to how to invest in the growth of these new societies is one we have outlined in many letters over the past 19 years: trust in management and national aspirations, but validate and verify the strategies and execution. 2025 was a year that showed the strength of our operating model, but challenged duration and conviction in what remains one of the most open economic areas globally. Openness invites innovation and growth, as well as competition and a certain myopia about terminal value among some economic actors.

The fundamental thesis that drove the establishment of Ajeej Capital in 2007: that the GCC lies not at the edge of the investable world, but rather at its 21st century nexus, evolved in important ways in 2025. Certainly, awareness of the region as a political and economic hub is greater than in any time in the past, and migration to the GCC outpaces, on a nominal basis (let alone on a growth basis), anywhere else on our planet from 2022-2025.

Thus, we see the headlines that trumpet ‘the end of globalisation’ as comically incorrect. While the Western world seemingly busies itself slamming shut doors to migration and investment and throwing up exciting new regulatory complexities, the rest of the world (which we will endearingly refer to as ‘Rest-ern world’ here on out) is merrily chugging along increasing synergies and deepening economic and social ties. How else to understand the 30 finalised and in process bilateral trade agreements (CEPAs) signed by the UAE since 2022 that stretch from Costa Rica to Malaysia to India and now to Kazakhstan. In 2025, we also saw Saudi Arabia codify its longstanding ties to Pakistan and Turkey in security cooperation agreements. As we all know, China successfully surpassed USD 1Tr in exports in 2025 despite a massive decline (tariff-driven) in US-directed exports.

China’s forced pivot away from its US customers in 2025 would not have been possible without trading cities like Singapore, Dubai, and the increasingly critical port infrastructure China controls or seeks to control in Vietnam, the Philippines, Indonesia, and beyond. Throughout this period, each of the governments in the GCC, and in fact across the broader region, played critical roles in enabling these growing South-South, East-South, East-East, Middle-South, Northeast-South flows. Dubai remains in the forefront, but in the past 5 years Abu Dhabi, Doha, and Riyadh have emerged as new global hubs for sophisticated commercial deals to be designed, signed, and executed.

And while the GCC cannot compete from a demographic perspective with the size of investment opportunities in India, or Indonesia, or broadly Sub-Saharan Africa, it’s important to remember that the GCC capitals already function as the de facto financial capital for tens of thousands of Indian, African, and Central Asian businesses This has spurred annual population growth in the region to well over 4% for the past several years (crossing 8% per annum in Dubai in 2024 and 2025,) and is set to continue, particularly as European and UK migration to the GCC accelerates with Western capital allocators migrating towards the location of both their investments and increasingly, their investors. Dubai, specifically, is increasingly a window into Africa as well as a launchpad into India and broader South Asia. The latter is obvious with millennia of active trade between the subcontinent and the Gulf, with Dubai and Muscat as the main ports. The connection with Africa is less obvious, until one understands that Dubai International Airport provides between 350 to 400 direct flights (depending on seasonality) to African capitals every week. This is effectively the same number as the aggregate of 4 major European airports - the total weekly flight count from Heathrow, Gatwick, Charles de Gaulle and Orly combined ranges from 370 to 450.

As we have noted previously, the surge in assets managed in the UAE is a major element in its growth as a services economy and increasingly as a data economy, particularly as investments in complex digital and consumer services as well energy-driven (AI) intelligence accelerate far beyond Silicon Valley. Incredibly, from less than USD 10B in locally managed AUM in 2010, today nearly USD 500B (almost AED 2T) in assets is managed out of the DIFC and ADGM, a 15-year CAGR of 48%. Those AUMs now reach a level of 83% of UAE GDP, up from <1% of GDP in 2011. The surge in human managers that accompany these assets, and that further support a broadening pyramid of services and consumption domestically are a core part of our investment thesis in UAE real estate, infrastructure, and consumer names.

As we outline below, the region’s natural resource wealth, paired with its commitment to energy investments and its foresight in growing power generation make it a critical home for compute, inference, and knowledge generation over the next decade and beyond. As a team with a few maths nerds, we share with you a transitive property derived power rule for the GCC in an AI-driven world:

In a world where scale and productivity gains are rapidly accelerating as a function of AI, beyond its location at the geographic and cultural centre of ‘Rest-ern’ trade, the GCC is also the place where fast, cheap, scale-able compute and the related productivity gains will happen fastest. That acceleration is very visible in every GCC capital city and is embraced by both the GCC resident populations as well as the GCC leadership. Why? Because structural barriers to innovation (limited local talent, limited local ability to ‘test’ ideas) are more easily scaled in 2026 than ever in the region’s history, given ample power resources and machine learning models.

Ajeej Annual Letter - Life at the centre of the 'Rest-ern' world

Read the full letter

Read the full letter\

Further Reading

\

Get the latest insights

We share perspectives, research, and market insights to help investors and founders see where growth is emerging — and how to capture it. Discover what others might be missing.

Investment Manager: Ajeej Capital (DIFC) Limited, regulated by the Dubai Financial Services Authority (DFSA). Ajeej Capital (AD) Limited regulated by the Financial Services Regulatory Authority (FSRA) of Abu Dhabi Global Market (ADGM). FSP No. 180021. © Ajeej Capital 2026